Infrastructure Week came and went with plenty of discussion about permitting reform, grid reliability, power demand, and America’s energy future.

But while Washington focused on the need to build energy infrastructure faster, the latest federal data shows where much of that buildout is happening. And it isn’t in Pennsylvania.

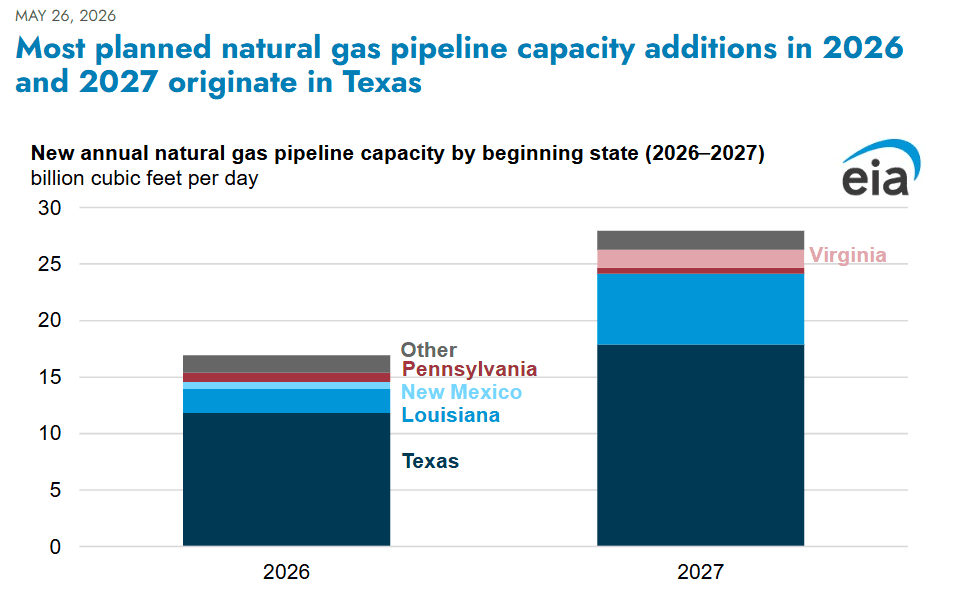

According to new data from the U.S. Energy Information Administration, developers plan to bring nearly 45 Bcf/d of new natural gas pipeline capacity online in 2026 and 2027. More than two-thirds of it originates in Texas, followed by Louisiana. Pennsylvania — one of the nation’s largest natural gas producers — is largely absent from that new buildout.

That should raise eyebrows. Pipeline capacity and energy costs have a direct relation. Just ask New York and New England who continue to have the highest energy costs in the greater Northeast. All because of obstructionist policies that shelve infrastructure projects.

Pennsylvania Is Already Powering the Region; Why Not Supply More of It?

Pennsylvania remains one of the most energy-rich states in the country, and there’s bipartisan agreement producing and using more of our homegrown natural gas is critical to long-term energy security.

The Commonwealth produces more than 7 Tcf of natural gas annually, ranks as the nation’s second-largest natural gas producer, and exports more electricity than any other state in the country. Natural gas fuels more than 60% of electric generation while using only a portion of the state’s annual production.

That reliability has helped stabilize electricity generation costs while supporting economic growth throughout the region.

At the same time, AI and tech infrastructure, advanced manufacturing, and broader economic growth are driving a new era of electricity demand. Grid operators, including PJM, continue warning that reliability margins are tightening as demand accelerates faster than new dispatchable generation comes online.

Considering the current prices of energy, the outlook on energy demand, and Pennsylvania’s abundant natural gas resources, one would believe it’s a no brainer to build the infrastructure necessary to get natural gas to market. They’d be wrong.

The Next Buildout

Where Pennsylvania’s loses out, Texas cashes in. Accounting for nearly 30 Bcf/d of planned new pipeline capacity additions over the next two years, Texas is looking to benefit in a big way. The projects are designed to move more Permian Basin natural gas to LNG export facilities, industrial users, power generation, and growing population centers.

Major projects like Rio Bravo Pipeline, Blackcomb Pipeline, and Hugh Brinson Pipeline are already under construction.

Meanwhile, Pennsylvania — sitting atop the prolific Marcellus and Utica formations — still has substantial opportunity to expand the infrastructure needed to fully meet rising domestic and global demand.

At some point, “energy leadership” requires actually building energy infrastructure, but that has proven difficult in the Appalachian Basin.

Infrastructure Delays Have Consequences

Infrastructure Week discussions repeatedly focused on competitiveness, permitting reform, and the need to accelerate project delivery timelines.

That matters for Pennsylvania because infrastructure constraints affect far more than producers. They impact consumers, manufacturers, grid reliability, investment decisions, and long-term economic growth.

Without adequate pipeline capacity:

- Natural gas cannot efficiently reach high-demand markets

- Reliability pressures increase during peak demand periods

- Consumers face higher energy costs

- Investment shifts to states that can build faster

“The economic potential of this resource can only be realized if government moves at the speed of business,” Marcellus Shale Coalition President Jim Welty said at a recent roundtable.

Thankfully, there are signs momentum may be shifting in a more constructive direction, at least at the federal level.

On May 21, the Federal Energy Regulatory Commission voted unanimously to advance the most significant reforms to its natural gas blanket certificate program since 2006. The proposed reforms would expand streamlined approval pathways for pipeline upgrades and related energy infrastructure projects while increasing the types of projects eligible for faster authorization.

FERC’s move comes as members of Congress – including Pennsylvania Senator Dave McCormick – continue pushing serious federal permitting reform that would minimize climate alarmists’ ability to obstruct access to the abundant domestic energy Americans increasingly depend on.

Pennsylvania Is Positioned to Lead

Pennsylvania’s advantages remain significant.

The Commonwealth has the resource base, workforce, geographic advantage, and existing energy infrastructure to remain a major player in America’s energy future. Pennsylvania’s natural gas industry supports more than 123,000 jobs statewide, while apprenticeship and workforce training partnerships continue creating pathways into family-sustaining careers.

Infrastructure Week reinforced a reality that is becoming increasingly clear: the states that are best positioned for long-term energy leadership will be the ones able to pair reliable energy production with the infrastructure needed to deliver it.

Pennsylvania already has the natural gas, workforce, and strategic location. Ensuring infrastructure growth keeps pace with rising demand is what will allow the Commonwealth to fully capitalize on that advantage.